Bitcoin for Retirement: Smart Investment or Risky Gamble?

Understanding Bitcoin as an Investment

Bitcoin is the first and most well-known cryptocurrency—a decentralized digital currency that allows transactions without the need for banks or governments. Lets see if Bitcoin for Retirement funds is a risky gamble or a sensible investment.

Introduced in 2009 by the mysterious Satoshi Nakamoto, Bitcoin operates on blockchain technology, a transparent and secure ledger that records all transactions.

Initially, Bitcoin had no real market value, but in 2010, a programmer famously exchanged 10,000 BTC for two pizzas. Fast forward to 2025, and Bitcoin’s price has surged close to $100,000 per coin—an astonishing rise of nearly 190,000,000% since its inception.

This meteoric growth has drawn the attention of both retail and institutional investors, fueling discussions about whether Bitcoin is a viable long-term asset, particularly for retirement planning.

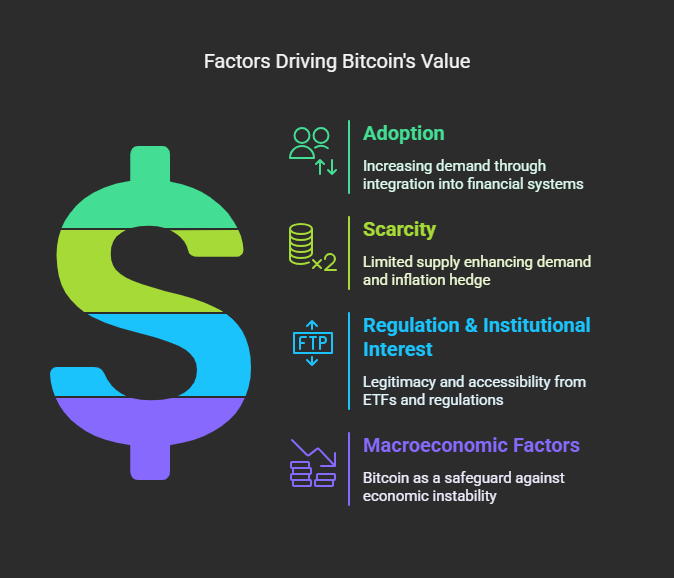

Why has Bitcoin Gained Value?

Bitcoin’s rise in value is driven by several key factors:

Adoption

Individuals, institutions, and even governments are integrating Bitcoin into financial portfolios, payment systems, and investment funds. As Bitcoin becomes more widely accepted, demand increases, contributing to price appreciation.

Scarcity

Bitcoin has a fixed supply of 21 million coins, making it a scarce digital asset. Unlike fiat currencies, which can be printed endlessly by central banks, Bitcoin’s limited supply drives demand and positions it as a hedge against inflation.

Regulation & Institutional Interest

The approval of Bitcoin exchange-traded funds (ETFs) in the U.S. has significantly boosted legitimacy and accessibility. With clearer regulations, institutional investors who previously hesitated due to legal uncertainties now have a safer and more structured way to gain exposure to Bitcoin.

Macroeconomic Factors

Economic downturns, fiat currency devaluation, and inflation concerns have reinforced Bitcoin’s appeal as a “store of value,” akin to digital gold. Investors view it as a safeguard against traditional financial instability.

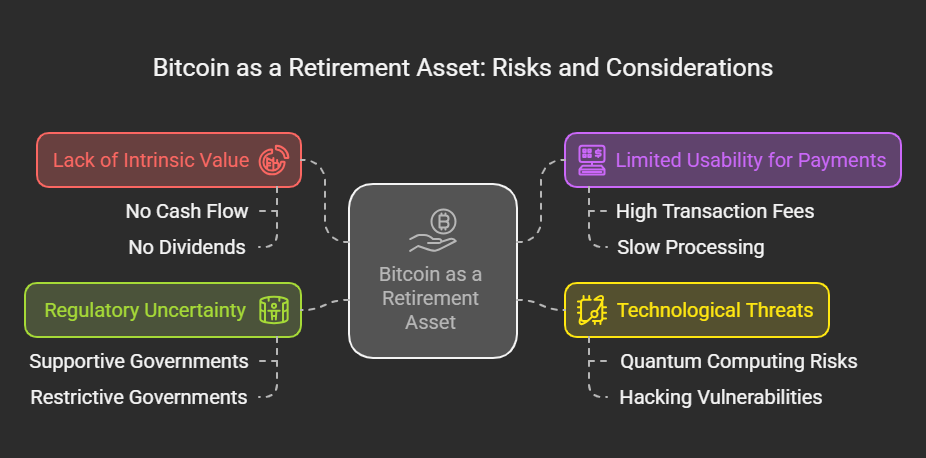

Bitcoin as a Retirement Asset: Risks and Considerations

Is Bitcoin Too Risky for Retirement?

Bitcoin has shown significant price appreciation, but its suitability as a retirement asset remains debated. Here are the key risks:

Lack of Intrinsic Value

- Financial experts, including Warren Buffett, argue that Bitcoin has no inherent value.

- Unlike stocks or real estate, it doesn’t generate cash flow or dividends.

Limited Usability for Payments

- Originally designed as a decentralized currency, but high transaction fees and slow processing make it impractical.

- Stablecoins like Tether (USDT) offer a more efficient alternative for daily transactions.

Technological Threats

- Advances in quantum computing could break Bitcoin’s cryptographic security.

- If this happens, transactions could become vulnerable to hacking, leading to a market crash.

Regulatory Uncertainty

- Governments have varying stances—some support Bitcoin, while others impose restrictions or bans.

- Stricter regulations could limit adoption and affect price stability.

Bitcoin’s Historical Volatility: A Cautionary Tale

Bitcoin’s price history is marked by extreme volatility, often seeing gains and losses exceeding 50% in short periods. Here are some notable crashes:

- June 2011: The Mt. Gox hack crashes Bitcoin from $32 to $0.01 (-99.9%).

- April 2013: Speculative hype drives BTC to $260 before plummeting to $50 (-83%).

- 2017–2018: BTC reaches $19,497 before crashing to $3,300 (-83%).

- March 2020: COVID-19 panic causes BTC to drop from $7,900 to $4,000 (-50%).

- May 2021: BTC hits $64,800 but quickly corrects to $30,000 (-50%).

- November 2022: The FTX collapse pushes BTC below $16,000, shaking investor confidence.

While Bitcoin has always recovered from these crashes, its history of drastic price swings makes it a risky choice for retirement savings.

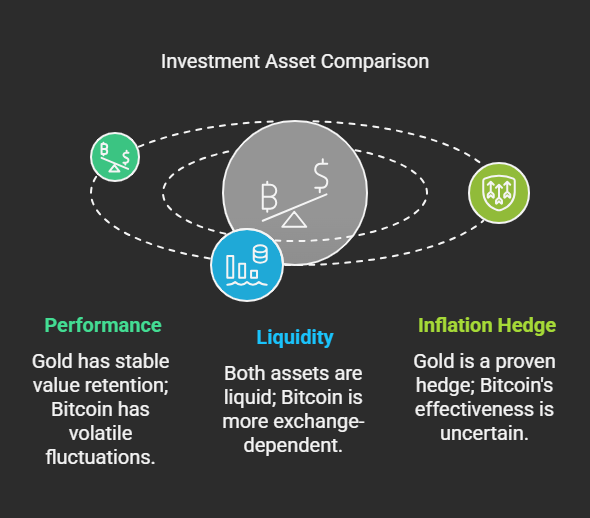

Bitcoin vs Gold: Which Is Better for Retirement?

For decades, gold has been considered a reliable retirement investment. Bitcoin, often dubbed “digital gold,” offers higher potential returns but comes with significantly greater risks.

- Performance: Gold has retained value over centuries, whereas Bitcoin has experienced wild fluctuations within months.

- Liquidity: Both assets are liquid, but Bitcoin is more susceptible to exchange failures, hacking incidents, and liquidity crises on trading platforms.

- Inflation Hedge: Gold has a proven track record as an inflation hedge, whereas Bitcoin’s short history makes its long-term effectiveness uncertain.

For investors prioritizing stability, gold remains the safer option. However, some diversify by allocating a small portion of their portfolio to Bitcoin, betting on its scarcity and growing adoption.

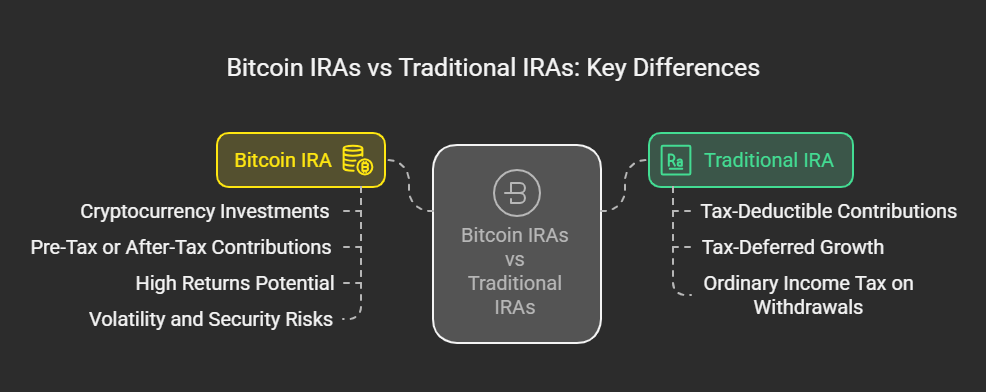

Bitcoin IRAs vs Traditional IRAs: Key Differences

Bitcoin IRAs allow direct cryptocurrency investments, whereas traditional IRAs focus on stocks, bonds, and mutual funds. Understanding the differences is crucial:

Traditional IRA:

- Contributions are tax-deductible, reducing taxable income.

- Investments grow tax-deferred, allowing capital to compound.

- Withdrawals in retirement are taxed as ordinary income.

Bitcoin IRA:

- Enables investment in Bitcoin and other cryptocurrencies, adding diversification.

- Contributions can be pre-tax (Traditional BTC IRA) or after-tax (Roth Bitcoin IRA).

- Offers potential for high returns but comes with extreme volatility and security risks.

- Vulnerable to exchange hacks and private key mismanagement, leading to possible irreversible losses.

Can Bitcoin Be Part of a 401(k)?

Some companies, such as Fidelity Investments, now allow employees to allocate a portion of their 401(k) to Bitcoin. This caters to tech-savvy investors who believe in Bitcoin’s long-term growth. However, regulatory agencies warn against the risks, emphasizing concerns about fraud, volatility, and inadequate consumer protections.

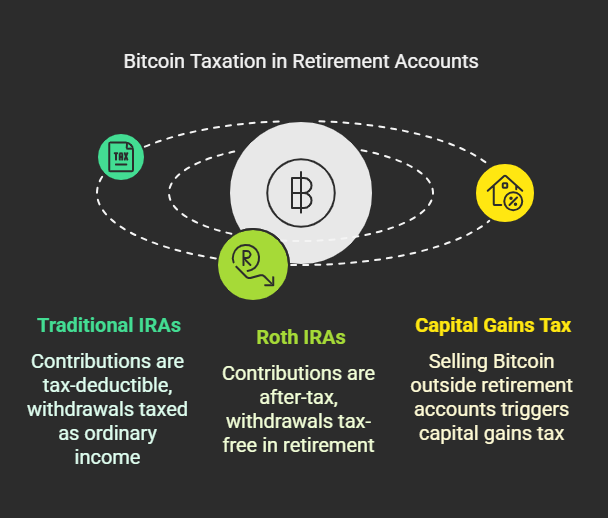

Tax Implications of Bitcoin for Retirement Accounts

Understanding taxation is critical when incorporating BTC into retirement planning:

- Traditional IRAs: Contributions are tax-deductible, but withdrawals (including Bitcoin gains) are taxed as ordinary income.

- Roth IRAs:Contributions are made with after-tax dollars, and withdrawals (including BTC gains) are tax-free in retirement, making them attractive for long-term crypto investors.

- Capital Gains Tax: Outside of retirement accounts, selling BTC triggers capital gains tax, which varies based on the holding period and tax bracket.

Final Verdict: Should you invest in Bitcoin for Retirement Portfolio?

Bitcoin presents an unprecedented opportunity for high growth, but it comes with significant risks. Traditional assets like gold and stocks remain safer choices for retirement, but a small allocation to Bitcoin could enhance diversification for those with a high-risk tolerance.

Investors should carefully weigh volatility, regulatory uncertainties, and security risks before committing BTC to their retirement plans.

Consulting a financial advisor can help tailor a strategy based on individual risk appetite and long-term goals. While BTC future remains uncertain, its potential to reshape finance makes it an asset worth considering—just not as the foundation of a retirement portfolio.