The Future of Money: How CBDC can reshape Digital Finance

What is a CBDC?

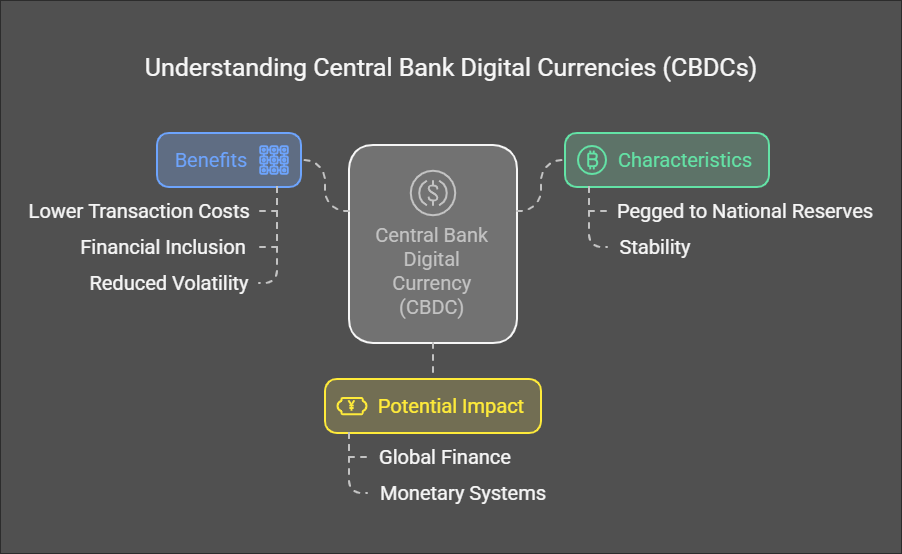

A central bank digital currency (CBDC) is a digital version of fiat currency issued and regulated by a central bank. Unlike decentralized cryptocurrencies, a CBDC is pegged to national reserves at a 1:1 ratio, ensuring stability while offering the efficiency and accessibility of digital assets.

CBDCs aim to provide:

- Lower transaction costs with instant processing

- Financial inclusion for the unbanked population

- Reduced volatility compared to traditional cryptocurrencies

This guide explores the fundamentals of CBDCs, their impact on global finance, and whether they can revolutionize monetary systems.

How Can Digital Technology Revolutionize Finance?

The world is rapidly moving toward a cashless society. In 2020, cash payments in the United Kingdom declined by 35%, with over 80% of global consumers shopping online. The transition to digital payments is fueled by:

- E-commerce growth – Projected to reach $6.5 trillion in sales.

- Declining use of physical cash – Digital transactions are becoming the norm.

- Convenience and security – Faster and safer payment options.

Given this shift, a bank-issued digital asset seems like the next logical step in financial evolution.

How do CBDCs Work?

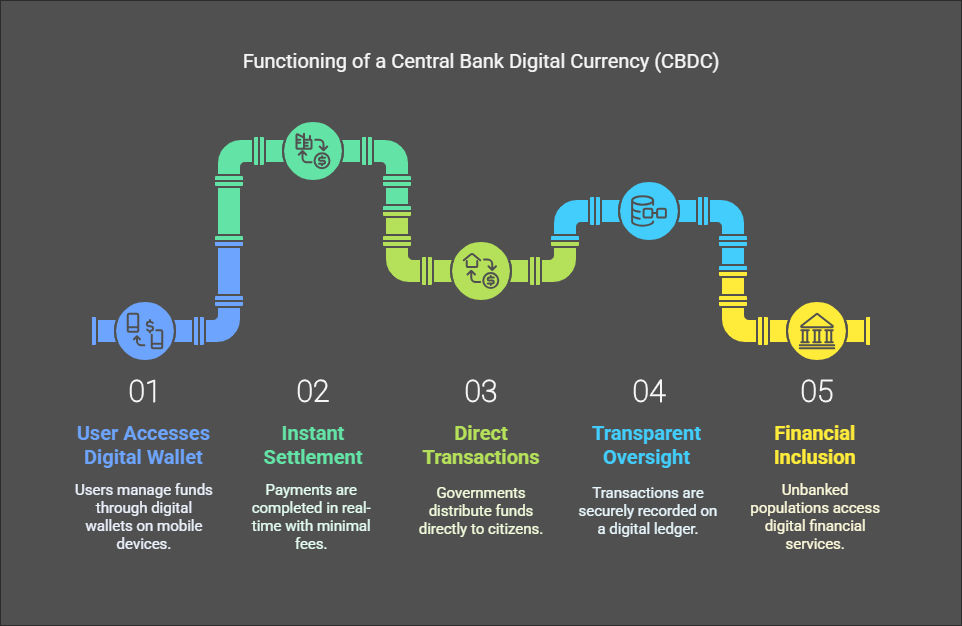

They functions much like traditional currency but exists solely in digital form. Users would manage their funds through digital wallets accessible via mobile devices. Unlike conventional banking, DCs leverage blockchain-based distributed ledger technology (DLT) to facilitate:

- Instant settlements: Payments can be completed in real-time with minimal transaction fees.

- Direct transactions: Governments can distribute funds directly to citizens without intermediaries.

- Transparent financial oversight: Every transaction is securely recorded on a digital ledger, aiding in fraud prevention.

- Financial inclusion: Unbanked populations can access digital financial services without needing a traditional bank account.

While blockchain technology ensures transparency, privacy concerns are addressed through permissioned networks, allowing central banks to control data access without making transactions fully public.

Key Differences Between CBDCs and Traditional Bank Accounts

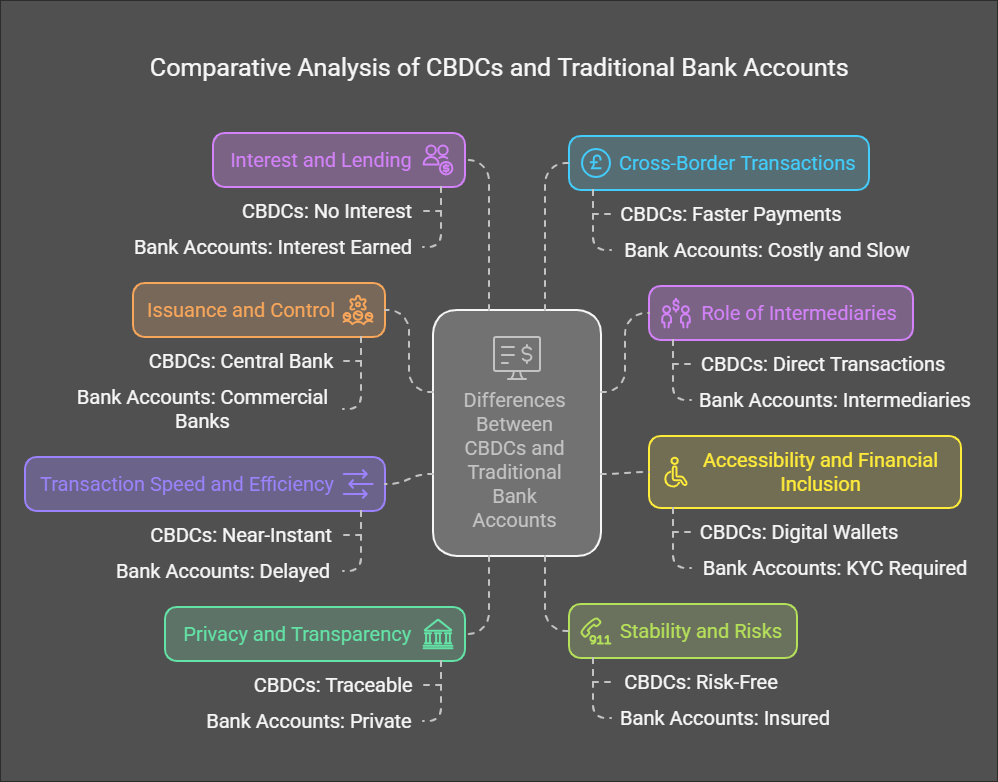

Issuance and Control

- DCs: Issued and controlled directly by the central bank.

- Bank Accounts: Managed by commercial banks under central bank regulations.

Role of Intermediaries

- DCs: Transactions occur directly without banks.

- Bank Accounts: Banks act as intermediaries for all transactions.

Accessibility and Financial Inclusion

- DCs: Available to anyone with a digital wallet, including the unbanked.

- Bank Accounts: Requires KYC verification and may have account maintenance fees.

Transaction Speed and Efficiency

- DCs: Near-instant transactions with minimal delays.

- Bank Accounts: Transfers can take hours or days, especially across borders.

Privacy and Transparency

- DCs: Fully traceable by the government, reducing financial crimes.

- Bank Accounts: Offers more privacy, but banks track transactions for compliance.

Stability and Risks

- DCs: Risk-free as they are directly backed by the central bank.

- Bank Accounts: Exposed to bank failures and liquidity risks, though deposits may be insured.

Interest and Lending

- DCs: Typically do not generate interest for holders.

- Bank Accounts: Earn interest on savings and enable lending activities.

Cross-Border Transactions

- DCs: Can enable faster and cheaper international payments.

- Bank Accounts: Costly and slow due to intermediaries and currency exchanges.

| Aspect | CBDCs (Central Bank Digital Currencies) | Traditional Bank Accounts |

|---|---|---|

| Issuer | Issued directly by the central bank. | Issued and maintained by commercial banks. |

| Control | Controlled by the government and central bank. | Managed by private or public banks under regulations. |

| Access | Can be accessed without a traditional bank account. | Requires an account with a commercial bank. |

| Transaction Speed | Near-instant transactions using blockchain or DLT. | Transactions can take hours or days, especially for cross-border payments. |

| Intermediaries | No intermediaries; transactions occur directly with the central bank. | Banks and payment processors act as intermediaries. |

| Interest Earnings | May not offer interest like savings accounts. | Savings and deposit accounts offer interest. |

| Privacy & Oversight | Fully tracked by central banks for financial monitoring. | Commercial banks track transactions, but with more privacy. |

| Security | High security due to central bank backing and blockchain use. | Secure but prone to bank failures or cyberattacks. |

| Usage Scope | Mainly for digital payments and financial inclusion. | Full banking services, including loans and investment options. |

| Deposit Insurance | Backed 100% by the central bank, reducing default risk. | Insured up to a limit (e.g., FDIC covers up to $250,000 in the U.S.).Future of DIgital Finance: CBDC Central Bank Digital Currency |

Pros and Cons of CBDCs

Advantages of CB Digtial Currency

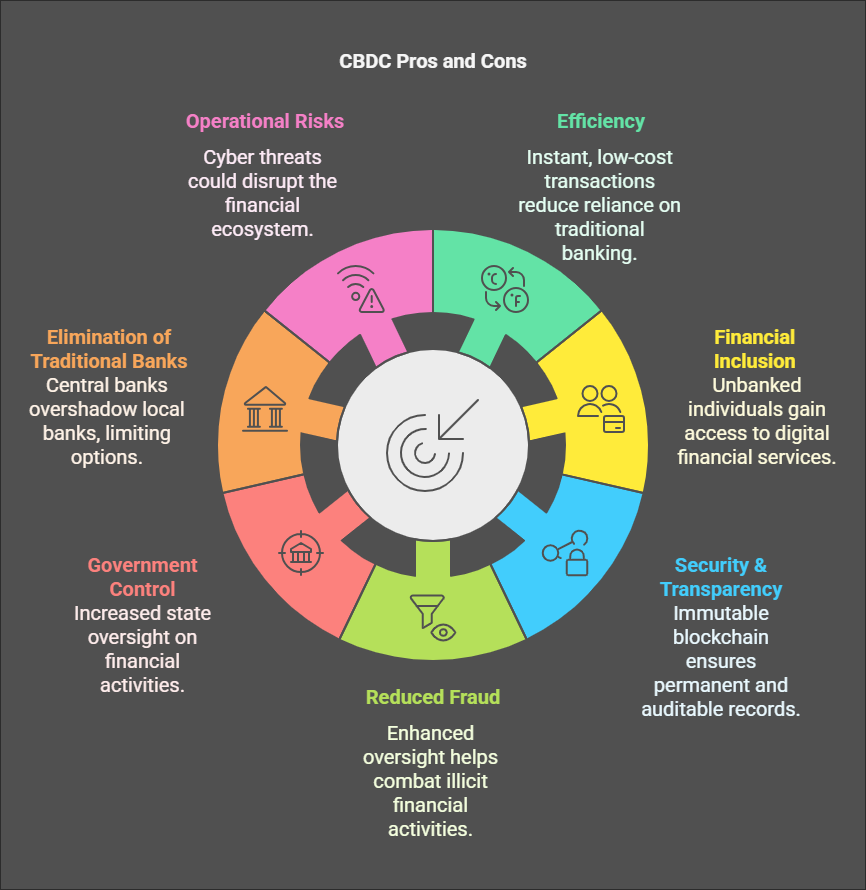

- Efficiency: Blockchain-backed digital currency facilitate instant, low-cost transactions, reducing reliance on traditional banking infrastructure.

- Financial Inclusion: Provides unbanked individuals with access to digital financial services without requiring a traditional bank account.

- Security & Transparency: The immutable blockchain ledger ensures transaction records are permanent and auditable.

- Reduced Fraud & Money Laundering: Enhanced oversight helps combat illicit activities by tracking suspicious transactions.

Disadvantages of CB Digtial Currency

- Government Control: Unlike decentralized cryptocurrencies, digital currency increase state oversight on financial activities.

- Elimination of Traditional Banks: With digital currency, central banks could overshadow local banks, limiting consumer banking options.

- Operational Risks: Errors or cyber threats could compromise the entire financial ecosystem, making it vulnerable to disruptions.

The Evolving Landscape of Regulation

United States:

Progress in the U.S. has been slower. In November 2021, the former chair of the Commodity Futures Trading Commission criticized the country’s “slow” and “expensive” payment systems, advocating for their rapid adoption to enhance efficiency.

Russia

The country is developing a digital ruble prototype and amending federal laws to support its implementation. A pilot program involving 12 central banks is underway, aiming for nationwide adoption.

Singapore

Known for its blockchain-friendly policies, Singapore is creating a retail DCs, which it describes as the “digital equivalent of today’s notes and coins.” This initiative aligns with the country’s push for financial innovation.

France

The Banque de France recently concluded a 10-month DCs experiment with 500 institutions. The trial involved issuing a digital currency for trading government bonds and security tokens, successfully testing settlement mechanisms.

China

A global leader in CBDC development, China has been working on a digital yuan since 2016 through its Digital Currency Institute. The currency, designed to replace cash payments, was made available to the public in April 2020.

Read - How RWA Tokenization is Revolutionizing TradFi

The Future of Central Bank Digital Currency

They are in different stages of development worldwide, but their widespread adoption hinges on regulatory approvals and technological progress.

Several critical questions remain, including whether foreign entities will have access to DCs and how taxation policies will be structured.

As financial systems evolve, CBDCs have the potential to create a more inclusive and efficient global economy by streamlining transactions, improving financial accessibility, and reducing reliance on traditional banking infrastructure.

Frequently Asked Questions – Central Bank Digital Currency

1. Will CBDCs replace cash?

No, CBDCs are designed to complement fiat currencies, not replace them entirely.

2. Are CBDCs the same as cryptocurrencies?

No, CBDCs are government-backed and centralized, while cryptocurrencies like Bitcoin are decentralized and not controlled by any authority.

3. What are the main risks of CBDCs?

CBDCs pose concerns related to privacy, government control, and potential banking disruptions due to disintermediation.

4. When will CBDCs become widely available?

While several countries are piloting CBDCs, mass adoption will depend on successful implementation and regulatory approvals over the coming years.